The Covid-19 pandemic has a growing negative impact on economies all around the world. In an earlier study, we estimated the possible output and employment effects of the Covid-19 pandemic in Turkey. Our predictions, based on an analysis using the 2012 IO table and the 2017 output and employment data, suggested that the non-agricultural labor demand in Turkey could decline by 19-29{4a62a0b61d095f9fa64ff0aeb2e5f07472fcd403e64dbe9b2a0b309ae33c1dfd}. If the decline in labor demand translates into unemployment, these figures imply that 4.2-6.5 million people could get unemployed because of the measures taken to limit the spread of Covid-19.

In order to reduce the impact of Covid-19 pandemic, we proposed a direct income transfer policy for those affected by the administrative measures. The proposed policy could cost around 4{4a62a0b61d095f9fa64ff0aeb2e5f07472fcd403e64dbe9b2a0b309ae33c1dfd} of GDP, and eliminate almost half of the decline in output and employment.

The Minister for Family, Labor and Social Services, Zümrüt Selçuk, tweeted that, as of April 27, 292 thousand companies applied for short term employment allowance for the benefit of 3.19 million workers. We will compare our estimates with those figures provided by Selçuk.

All employees are not eligible for short term employment allowance (STEA). The eligibility conditions have been somewhat eased because of the Covid-10 pandemic. A worker is eligible for STEA only if she paid unemployment insurance contribution for at least 450 days in the last 3 years, and was employed in the last 60 days prior to the application. It does not cover non-registered workers, self-employed, unpaid family workers as well as those registered workers who do not satisfy the minimum requirements (450-days and 60-days conditions).

An unprecedented level of unemployment

In order to compare our predictions with that of realization, we need to estimate the number of eligible workers. We assume that registered wage earners on a permanent contract employed before 2017 are eligible for STEA, and calculated labor demand effect for these workers.

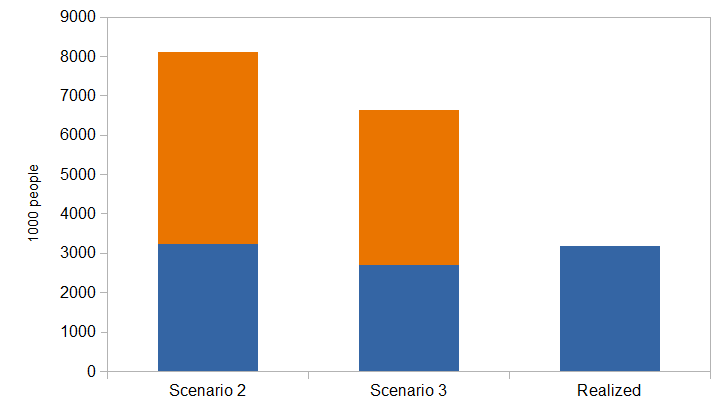

Note: The blue bar represents workers eligible for STEA, and the orange bar non-eligible employees. The “realized” bar shows STEA applications as of April 27.

Figure 1 shows the data on the estimated decline in labor demand (in terms of the number of workers/employees) for Scenario 2 and 3, and the number of applications for STEA. The results for Scenario 1 are not presented because that scenario now looks like unrealistically optimistic. The blue parts for scenarios represent those workers who are assumed to be eligible for STEA, and the orange part non-eligible employees.

The aggregate results are quite similar: there are 3.19 million workers applied for STEA as of April 27, whereas the “realistic” and the then “pessimistic” scenarios predict, respectively, that 2.69 and 3.24 million “eligible” non-agricultural wage earners could get unemployed, excluding policy response. By any standards, this is a huge and unprecedented loss in employment. Unfortunately, the real loss in employment is even more than that. According to our estimates, the number of non-eligible workers who could lose their jobs is around 3.9-4.9 million. In other words, the STEA applications may represent only less than half of real losses. It is assumed that those employed before 2017 would be eligible because the 2017 Labor Force Survey data are used. In order to compare 2017 and 2019 employment data, it should be mentioned that the number of non-agricultural wage earners was almost the same in those years: 18.4 million in 2017 and 18.7 million in 2019, according to the Turkish Statistical Institute (TUIK) figures.

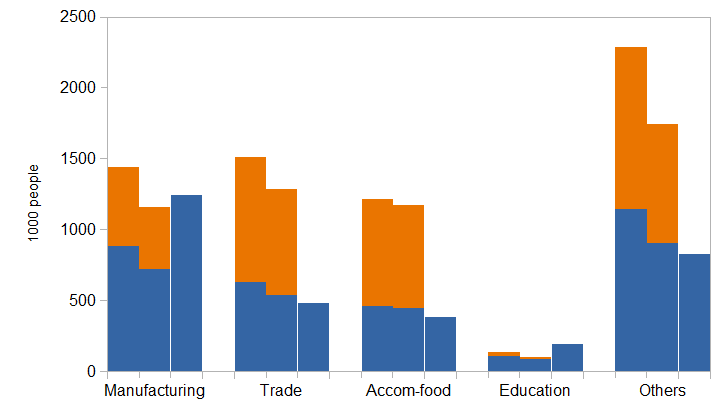

Note: The 3 bars for each sector show Scenario 2 and Scenario 3 predictions and the real figures, respectively. The blue bar represents workers eligible for STEA, and the orange bar non-eligible employees.

The data at the sectoral level is presented in Figure 2. With the exception of manufacturing, the number of applications is quite close to the predictions of Scenario 3. For manufacturing, the number of applications is even much higher than the case under the the most pessimistic scenario.

Not an optimistic outlook

We can summarize our observations as follows:

* The economic impact of the Covid-19 pandemic is substantial. It causes huge employment losses. Although administrative measures aimed at social isolation restricted mostly the service sectors like accommodation and food, travel, retail trade, etc., the (unexpected) sharp decline in manufacturing employment is worrisome.

* The data on STEA applications reveal only a (small) part of the (employment) problem. There are millions of unregistered workers, self-employed people, and unpaid family workers who lost their jobs and income.

* The policy response is too slow and too small. The STEA excludes a large part of employees. Moreover, only 43{4a62a0b61d095f9fa64ff0aeb2e5f07472fcd403e64dbe9b2a0b309ae33c1dfd} of applicants have received support so far (the total number of STEA recipients was 1.4 million in April 27). Finally, direct income support accounts only a small fraction of the support program, and most of direct income support is provided only once.

* In order to reduce the social and economic cost of the Covid-19 pandemic, direct income support should be provided unconditionally and rapidly to the extent that covers income losses of all those affected. There should not be any uncertainty about the extent and duration of the support because the uncertainty is one of the major factors that deepens the crisis.