In the inflation report that came on April 30, Turkish Central Bank (CBRT) revised its inflation forecast for 2020 from 8.2 percent to 7.4 percent. The forecast for 2021 is kept constant at 5.4 percent.

How realistic is this revision? In the short run, the downfall in demand and the fall in oil prices may dominate the upwards pressures coming from the exchange rate. In the medium to long run however, I am afraid that the upside risks to the long-term inflation outlook are underestimated.

Since the outbreak of the COVID-19 pandemic, central banks around the globe rapidly slashed their policy rates to provide the necessary stimulus. Because the policy rates were already at very low (even negative) levels in advanced economies, these central banks quickly increased the magnitude of asset purchases through Quantitative Easing (QE) programs and increased the amount of liquidity in the system.

Central Banks in emerging markets do not have the flexibility and the resources that are available to their counterparts in advanced economies. Neither do they have the credibility that is necessary to inject large sums of money without triggering inflationary expectations. Thus, they need to be more cautious. This is because if it is not implemented properly, a rapid increase in the domestic money supply may further destroy the weak credibility and trigger inflationary expectations.

Where does Turkey fit in this picture?

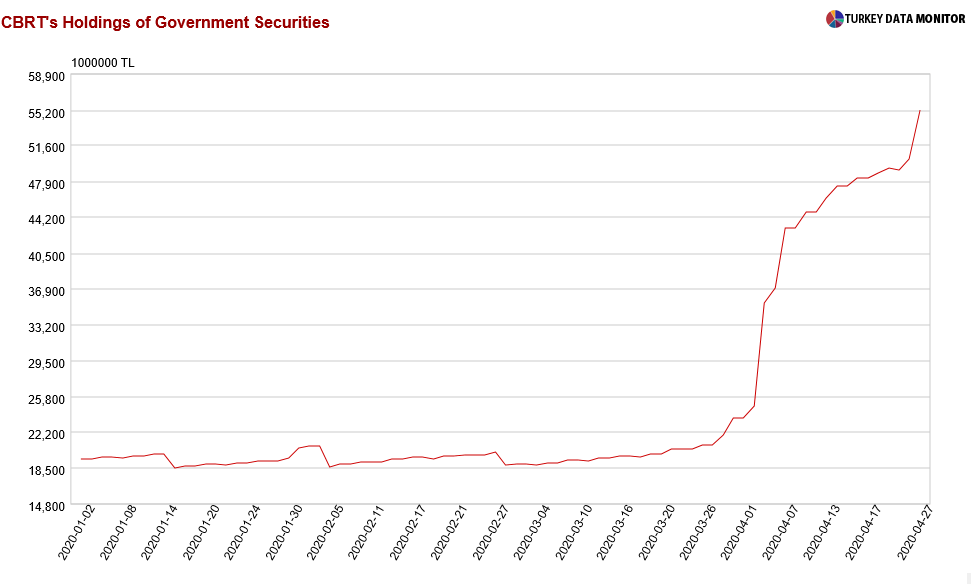

The CBRT announcement that came on March 31 relaxed the limits of bond purchases (which was previously stated to be 5 percent of the balance sheet) by noting that the limits “may be revised depending on the market conditions”. On April 17, the limit was clarified to be 10 percent. What happened after these announcements?

The figure shows CBRT’s holdings of government bonds. The rapid increase in securities holdings after March 31 reflects the sizable asset purchases after this date. One can understand why CBRT injects liquidity into the system at a time of crisis. Indeed, in an earlier piece, I had argued that money printing could be an option to offset COVID-19 crisis. What I had emphasized back then, however, was that even though money printing might be unavoidable, it should be executed properly with well-defined priorities and clear communication. It is essential to drain the money once inflationary pressures kick in.

Unfortunately, the recent practice suggests that this is not quite the case. What can go wrong? Let me elaborate, based on our recent research with Cem Çakmaklı, Sevcan Yeşiltaş, Şebnem Kalemli Özcan and Muhammed Ali Yıldırım.

QE vs Debt Monetization

In a QE, the central bank prints money and buys sizeable amounts of government bonds. How is debt monetization different? A central bank typically purchases securities through open market operations to meet the liquidity needs, consistent with its goal of price stability. The technical difference between money printing through an open market purchase and monetizing the debt is slim. Thus, some argue that QE policies are effectively debt monetization.

The Federal Reserve begs to differ and argues that debt monetization refers to a “permanent” source of funding for the government by the central bank and separates QE policies from debt monetization. So long as the central bank commits to inflation targeting and normalizes its balance sheet when inflationary pressures kick in, asset purchases in the form of QE are not considered debt monetization.

Hence, using the Federal Reserve’s usage of the term, the criterion for bond purchases to be considered debt monetization is whether the central bank fails to drain the money effectively later on and the money remains in the system permanently such that it leads to inflationary pressures.

In advanced economies, the distinction between QE and debt monetization can be easier to ascertain where the inflation rate is well-anchored and central bank credibility is well established. In fact, the inflation rate has not increased in US or Europe in the aftermath of large-scale quantitative easing policies after 2010.

The distinction between QE and debt monetization gets blurry in the context of an emerging market like Turkey, however, where central bank credibility is shaky and price stability is not well established even though Turkey has adopted inflation targeting as early as 2003.

If not drained at the right time…

The above discussion suggests that in order for QE to be a viable policy alternative in Turkey, it should be distinguished from debt monetization that leads to an increase in inflation. The key to successful monetary financing is policy credibility. Unfortunately, Turkey scores low on this. A badly managed QE will erode whatever credibility the monetary policy making has left in Turkey and de-anchor inflation expectations further, which would only escalate the existing crisis by pushing the inflation rate on a higher trajectory, increasing dollarization, and causing sharp depreciations in TL.

If it is not executed properly and the money is not drained from the system at the right time, QE can turn into inflationary debt monetization. The rapid increase in the monetary base combined with the increase in CBRT’s bond holdings is concerning in this regard, because it suggests sizable bond purchases in the absence of a well-defined QE program.

In order to prevent QE from turning into debt monetization, bond purchases that are part of COVID-19 crisis should be clearly communicated to the public. Furthermore, the coordination between monetary and fiscal policy should be transparent. The government should announce how the funding through bond issuance is channeled back to the economy and how long the program will last. Clear communication of a rigorous program is essential to enhance credibility and keep inflation expectations under control.

Last but not least, different from the advanced economy counterparts, a successful QE in an emerging market necessitates foreign currency inflows. Otherwise, the money that is printed in the system may trigger demand for foreign currency and cause further depreciations in the TL. An agreement that grants sizable currency inflows will also enhance the credibility of the program and disable the path that leads to monetization.