Selva Demiralp

Turkish growth figures that were released on Feb. 28 indicate that the fourth quarter growth was 6 percent while the annual growth rate for 2019 as a whole was 0.9 percent. When we take a look at the components of growth, we note that the driving forces were consumption and public spending. The decline in investment has slowed down, which is positive. Nevertheless, it is doubtful that this trend will continue going forward.

The recent developments in Syria are rather concerning from an economic perspective as well. The increase in the geopolitical risks would significantly hamper the GDP. If the tensions persist, it would further deteriorate the investment climate in Turkey that barely showed signs of improvement in the last quarter. Similarly, if the rapid depreciation in the exchange rate turns out to be permanent, it would push the inflation rate up, lower aggregate demand and increase market interest rates, which may lead to significant financial instability. I wish a diplomatic solution will be reached soon and the geopolitical risks will be off the table. Nevertheless, the outlook for economic growth would still be somewhat cloudy looking forward.

What kind of growth?

The important issue that needs to be emphasized about economic growth is the quality and the sustainability of growth. Economists do not welcome all kinds of growth. This is perhaps the most fundamental point where we disagree with the politicians. A strategy that aims to maximize short run gains by all means might allow the politician to win the elections. But it will not be sustainable. And it will cause more damage to the economy in the long run.

An experienced coach does not ask a marathon runner to run as fast as she can. If the athlete runs at her maximum speed and pushes her body to her limits, she collapses mid-way and cannot complete the race. In a similar vein, an economist does not ask for maximum growth because periods of high growth beyond potential cause overheating and subsequent slowdown. The recovery that follows is subject to many unknowns. The inflation that results from overheating is typically permanent and does not return to previous levels. This increases vulnerabilities looking forward and reduces growth.

As a result, the ideal growth rate from an economic perspective is the “potential growth rate,” which can be described as the long term average growth rate in an economy. It is sustainable and allows for more production in the long run. Because it does not increase the vulnerabilities and watches for macroeconomic balances, a growth rate that hovers around the potential increases the investment appetite and has the capacity to increase the potential growth rate. Thus, you can run faster without losing your breath.

Long term costs of short run gains

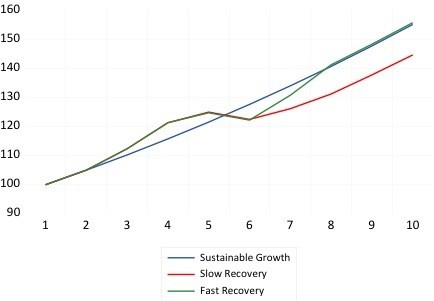

I illustrate three scenarios in the figure below. In all three scenarios, the starting point is 100 units of production. The blue line shows sustainable growth. In this scenario, the Gross Domestic Product (GDP) grows at 5 percent per year. Thus, at the end of ten years, the economy reaches the capacity to produce 155 units. The red and the green lines illustrate the scenarios where the policy makers are not content with the potential growth and promote policies to accelerate growth further. Post-2017 period can be an example for such a period where the annual rate reached 7.5 percent thanks to many support programs and subsidies.

Let’s now recall what happened in the period after 2017. How come we could not maintain the 7.5 percent growth rate? Such a high growth rate was achieved with significant credit growth and borrowing. In a country like Turkey where the domestic savings are low, high growth typically gives rise to external borrowing and increases our sensitivity to foreign exchange. Thus, any trigger may lead to significant financial fluctuations.

Now let’s recall what happened in the period after 2017. How come we could not maintain the 7.5 percent growth rate? Such a high growth rate could only be achieved with substantial credit expansion and borrowing. In economies like ours, which have low savings rates, funding needs prompt external borrowing and increase the reliance on capital inflows. As the Exchange rate becomes more fragile, any trigger can lead to sharp volatility in financial markets.

Indeed, this is what we experienced in the post-2017 period. Starting with 2018, the steady increase in the inflation rate and the depreciation in TL were the expected symptoms of an overheated economy. Pastor Branson crisis was the breaking point, which triggered the Exchange rate crisis that was followed by a recession.

What happens next?

The question at this stage is the speed of the recovery going forward. Assuming that the 0 percent growth rate in 2019 is the trough, will the economy go through a slow recovery path as shown by the red line, or will it go through a fast recovery as shown by the green line in the post-2020 period?

The ”V-shape” recovery that is shown by the green line necessitates a growth rate around 7-8 percent, similar to the period after 2009 recession. This is not very likely at this time because 2009 recession was merely the reflection of the global financial crisis in Turkey. It was not due to our vulnerabilities. Our external borrowing was at relatively reasonable levels. The private sector did not suffer balance sheet problems. There were no pressures on the Exchange rate. On the contrary, abundant liquidity injections by the Federal Reserve had already started. The sharp decline in demand dragged the inflation rate down to 6.5 percent. The budget deficit was low. Hence there was room for accommodative monetary and fiscal policies, which allowed us to recover quickly without generating further macroeconomic imbalances and increasing our risk.

In the period after 2018 recession, the slow recovery scenario that is shown by the red line seems more likely. The red line illustrates a growth rate around 3-4 percent after the trough. Even though you catch 5 percent growth afterwards, the GDP remains significantly below the levels achieved by the sustainable growth path at the end of 10 years. Thus, the gap between the red and the blue lines can be viewed as the long-term costs of policies that focus on short term growth.

Why is this scenario more likely? Different from 2009, we face a significant exchange rate and inflation problem at this time. Lowering the interest rates to stimulate the economy causes further depreciation of the Turkish Lira and increases the inflation rate. In turn, this drags investment and consumption down. The wider budget deficit due to expansionary fiscal policy last year leaves little room for further fiscal expansion at this time. Hence, the monetary and fiscal policies have limited capacity to stimulate the economy. Furthermore, the nonperforming loan problem that we inherited from the exchange rate crisis in 2018 limits the supply and demand for bank loans. If we add the geopolitical risks in Syria and the potential decline in global demand due to coronavirus, we can clearly argue that the downward risks to growth dominate the foreseeable future.