The flow of funds fuels the economy. By bringing together the borrower and the lender, financial markets direct savings into the economy. Savings finance production, production generates more income and hence more savings. What enables this circular flow is the payment to the saver. In modern financial systems, the saver receives an interest payment in exchange for lending. From the lender’s perspective, the interest rate is the cost of delayed consumption. What exactly is that cost?

Suppose you have 100K TL. You want to decide between buying a car and starting a transportation business or depositing your money in a bank. If you choose to deposit your money for a year, you calculate the approximate return from the transportation business first and demand a guaranteed return that is not too far off from this expected return from your bank.

Two dimensions of return

The return that you demand from your bank has two dimensions. The first dimension is the inflation rate. Assume that the inflation rate is 10 percent, and the car prices increase proportionally to the inflation rate. You must receive at least 110K TL next year to maintain the purchasing power of your savings. The second dimension is a real return that is proportional to the expected profits from the transportation business. This additional return over the inflation rate is the real interest rate.

The payment you will receive next year should include inflation compensation to allow you to purchase a car and the opportunity cost that you incur through foregone business opportunities. The sum of these two components is the nominal interest rate that your bank pays. If the bank’s interest rate is less than your calculations, it makes more sense to spend the savings today and buy a car rather than depositing the money in the bank. Under these conditions, people prefer consumption over savings.

One of the main reasons people avoid TL deposits lately is that the nominal interest rates are below the inflation rate. Hence, people prefer consumption or alternative means of savings through foreign exchange or gold deposits. If this becomes systematic and the real return from foreign exchange or gold deposits vanish as well, then the motivation to channel savings into the banking system would disappear, and financial markets would come to a halt, generating more risk and fragilities.

Participation banking

As described above, the interest rate aims to remove the savings from under the pillows and channel them into the financial markets to start the flow of funds that enable production and growth. The interest rate is the cost of using funds.

Continuing the example above, suppose instead of lending 100K TL to the bank, you purchase a brand-new car and lend it to a company. The following year you receive a brand-new vehicle based on your agreement. This type of arrangement is not against Islamic principles. If the company who borrowed the car uses it in the transportation business and gives you a share from its profits, that is not against Islamic principles either. This concept, profit sharing, is the foundation of participation banking.

At this point, the choice between a conventional bank and a participation bank can be described as follows: If I deposit my 100K TL to a conventional bank, the bank guarantees, say, 12 percent interest payment. Alternatively, if I deposit my money in a participation bank, I might earn more than 12 percent or less than 12 percent depending on their profitability.

The profit-sharing system

The main distinction between conventional banking and Islamic banking is that the payment is in the form of “profit-sharing,” and hence there is no guarantee; there is a risk of loss. On the other hand, if the funds are invested properly and in the absence of extraordinary events, participation banks can almost guarantee a profit as well. As we look at participation banking in Turkey practice, we note that even though the profit shares have fluctuated over time, participation banks did not register net losses and did not charge their customers for their deposits. Indeed, it is not surprising that conventional and participation banks’ profits are similar, given that they work in the same industry.

Our work with Seda Demiralp from Işık University the profit payments of Islamic banks with interest payment of conventional banks. We find that these alternative rates of return follow a similar trend and the profit share follows average interest payment with about a two-month lag. This finding is supported in the literature as well. (*)

As the Muslim population increases…

From the perspective of the saver, conventional banks and participation banks represent two alternative forms of investment. Our findings show that interest rate sensitivity of deposits in these alternative forms is not statistically different. Because participation banks are preferred due to religious beliefs, it is understandable that the average profit payment is somewhat below the average interest payment. That being said, if the gap between interest payments and profit shares increases, we observe that conservative savers exhibit rational behavior and switch to alternatives such as gold, foreign exchange, or real estate to route their savings. Hence, it is not feasible for participation banks to offer significantly lower profit payments and coexist with conventional banks.

As we evaluate the topic from this perspective, we note that the profit share and interest rate are closely integrated concepts. The share of Islamic finance is about 1 percent of global investment. In Turkey, this share is closer to 5 percent. As the Muslim population increases, this share may increase over time. Nevertheless, even if the share of Islamic finance increases, it would not cause a radical change in the workings of the financial system that brings together the borrower and the lender. The basic principle of financial markets does not change; it is impossible to borrow without a cost, and those costs generally move together whether it is in the form of interest payment or profit share.

How to reduce costs of borrowing

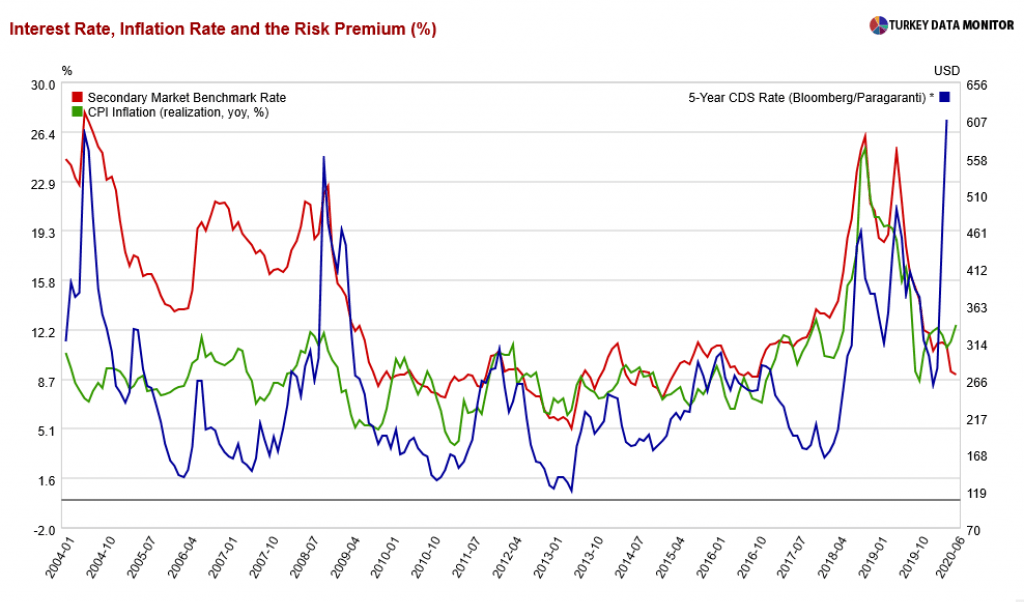

While it is impossible to borrow without a cost, it is possible to lower the costs of borrowing. The two fundamental determinants of borrowing costs are the inflation rate and the risk premium. The healthy and the sustainable way to lower borrowing costs is to achieve price stability. When price stability is achieved, borrowing costs can be reduced further by signaling credible policy and lowering the risk premium.

The figure illustrates that periods of lower inflation (the green line) are associated with lower market rates (the red line). Furthermore, periods of lower inflation generally correspond to lower risk premium (the blue line). This is exactly why the western economies enjoy low market interest rates.

Trying to lower borrowing costs in the absence of a decline in the inflation rate is not sustainable, however, due to the imbalances that it generates. The recent increase in the inflation rate as well as the Central Bank of Turkey’s poorly communicated quantitative easing (QE) policy is a concern in this regard because it signals that the current low interest rate environment is not sustainable.

(*) Korkut, C. ve Özgur, Ö. (2017). Is there a link between profit share rate of participation banks and Interest rate? The case of Turkey, MPRA Paper no: 81642

Çevik, S., ve Charap, J. (2011). The behavior of conventional and Islamic bank deposit returns in Malaysia and Turkey. IMF Working Papers, 1-23.

Ergeç, E. H., ve Arslan, B. G. (2013). Impact of interest rates on Islamic and conventional banks: the case of Turkey. Applied Economics, 45(17), 2381-2388.

Saraç F.ve Zeren M. (2015) The dependency of Islamic bank rates to conventional bank interest rates: Further evidence from Turkey, Applied Economics , 47 (7), 669-679.