As the cost of living increases, Turkey’s government took measures such as VAT reductions. Nonetheless, inflation cannot be reduced with tax cuts unless the reasons that escalate it are eliminated. Early this week, the VAT rates on some basic goods were reduced from 18 percent to 8 percent. A similar practice was applied for some other goods and services in mid-February. As the cost of living gets higher, such measures come one after another. So, is it possible to reduce inflation solely by reducing VAT? The right question is if inflation would abate only with VAT reductions without eliminating the causes that drive inflation.

Softball question. Hence, the answer is clear: In short, “no.”

What if the VAT rates were cut on all goods and services?

Let us do a straightforward analysis. Assume that the VAT of each good and service is reduced at the same rate. Although VAT is not the same for all goods and services, so be it; have a wide-ranging VAT reduction of 9.26 percent (the discount rate when reduced from 18 percent to 8 percent). Let us suppose that this discount was made at the beginning of September 2021 and all goods and services producers reflect this discount on their prices.

On the other hand, let other factors that determine the price of every good and service (exchange rate, labor, energy without VAT, imported input prices in foreign currency, profit rates, and the like) be unchanged as of September. Subsequently, the exchange rate or wages do not alter because the VAT has been reduced. In this case, the annual inflation rate would be lower from September 2021 onwards.

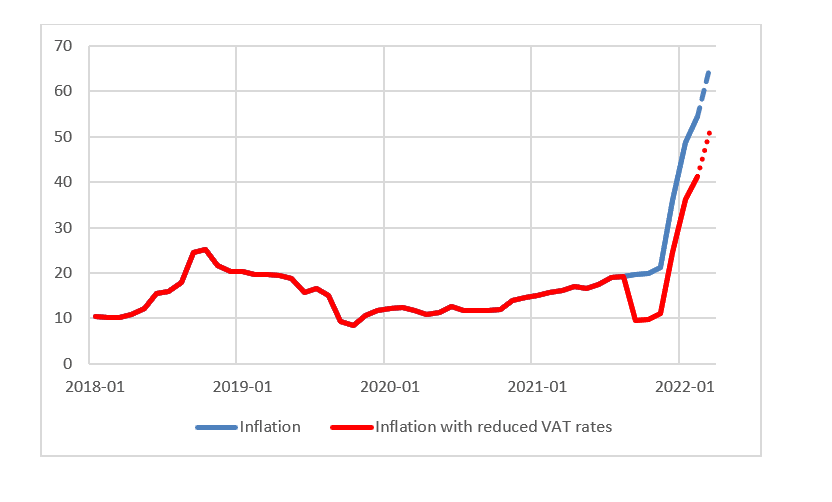

The inflation after the VAT reduction and observed inflation starting from January 2018 are displayed in Graph 1 to illustrate the historical change better. The March figure has not been announced; nonetheless, let it be 65% without a VAT discount.

Graph 1. Consumer inflation: January 2018-March 2022 ( percent annually, March value is predicted: dotted lines)

There would be temporary reduction in inflation

A general VAT reduction first brings down the annual inflation. Then the annual inflation follows a path parallel to the situation in the absence of a VAT reduction. Inflation in Graph 1 is annual. In other words, it displays how much the consumer price index of each month has increased compared to the consumer price index of the same month of the previous year.

In order to see the inflation compared to the previous month, if monthly inflation were plotted, inflation would have a negative value in a single month, and nothing would change in the following months. In September, the monthly consumer inflation was 1.25 percent, and it would be -7.3 percent with VAT reductions. Subsequent monthly inflations would remain at the same level before the reduction.

VAT reduction’s budgetary impact

VAT reductions are a burden on the budget. Evidently, lowering the VAT rate to make a commodity cheaper while raising the VAT on another item, such as a luxury one, can compensate for the reduced tax revenues. After all, this is a political choice.

Nonetheless, there is no way out: the cost of living cannot simply be dealt with by reducing tax rates. Continuous tax rate cuts simultaneous with a rise in inflation will deteriorate the budget. Eventually, this means more borrowing, more interest payments, less non-interest spending—less social transfer expenditures, for instance.

The 4-H’s policy

What has led us to this point? Starting from September 2021, the CBRT lowered the policy rate by five percentage points. The policy rate remained at 14 percent since the last reduction on 17 December. Thus, the 4-H’s policy came into play; High-interest rate, High exchange rate, High risk, and High inflation.

The following figures demonstrate the above-mentioned 4-H policy: 5-year Treasury bond yield in January: 25 percent (September average: 18 percent), average dollar rate in January: 13.5 (September average: 8.5). average risk premium (CDS) in January: 554 (September average: 378.5). inflation in January: 49 percent (September: 19.6 percent).

As can be observed, I compared the figures for January with September; hence, the Russo-Ukrainian war has no effect on the data. Moreover, instead of September 2021 figures, January or February 2021 figures could be considered. What is the deal with these months? They were the months when the previous CBRT Governor was not discharged, and the CBRT tried to fight inflation.

In that case, the 4-H’s policy would come out even more dramatically. Nevertheless, there is no need since the situation is crystal clear. Additionally, about a week ago, the Treasury borrowed in dollar terms with an 8.6% interest rate in international markets -a tremendous rate.

The intention was noble

The adventure that has ended with 4-H’s started with good intentions. We would turn the current account deficit into a current account surplus. We would do this by keeping our currency at a competitive level (by lowering the value of our currency – raising the exchange rate). Thus, on the one hand, our industry would tend to export more; on the other hand, some of the imported goods would be produced domestically.

There would be a structural transformation in increasing our foreign exchange income. In the same period, accommodation and similar services would attract more tourists, as it would be cheaper for foreigners. Our tourism income would increase, and our foreign exchange earnings would soar.

There could be some inflation in the meantime. So be it. As a result, our foreign debt would decrease with this structural transformation. Besides, the exchange rate would calm down after a while, and inflation would wither away. Moreover, we would be doing a structural change by lowering the value of our currency without going through the trouble of making structural reforms.

Winners vs. losers

After all, here we are. Corporations that use loans are gratified: They borrow at an interest rate below inflation. However, the price of the goods and services they sell rises as much as inflation, more or less. Banks are blissful: they borrow with 14 percent – 17 percent and lend loans with interest rates up to 30 percent, they make quite a profit.

Since giving without taking is peculiar to God, at least one group must be losing out on this circumstance. The losers are the savers and the Treasury. The deposits of those out of the exchange rate-protected deposit system have melted away due to rising inflation. On the other hand, for those participating in the currency-protected deposit system, the exchange rate must increase more than the annual inflation rate and the interest rate of 17% so that their savings would not erode due to escalating inflation. If so, then the Treasury would lose.

Increasing the current account deficit

Hold on a second. The current account deficit is equal to the difference between investments and savings. Our investment/GDP ratio has been around 4 percentage points below developing countries for the last ten years. However, our savings rate is about 8.5 percentage points below developing countries. In other words, our savings are not sufficient to finance these investments below the average. We are facing a significant current account deficit, and we are dependent on foreigners’ savings – that is, external borrowing.

So, where are we now? We took this path to turn the current account deficit into a current account surplus. Nonetheless, we have caused “High-interest rate, High exchange rate, High Risk, and High inflation.” Against the rising cost of living, with VAT reductions, we have implemented a practice that reduces inflation only once, then resumes and potentially disrupts the budget. We have penalized domestic private savings and reduced public savings (by distorting the budget).

In other words, we increased the current account deficit, and the hunter became hunted.

")